If you are reading my blog for the first time, read the below article first before coming back here

Especially when your loan interest (6%) from insurer is higher than your expected investment return (5%) ?🤨🤨🤨

Let’s see…

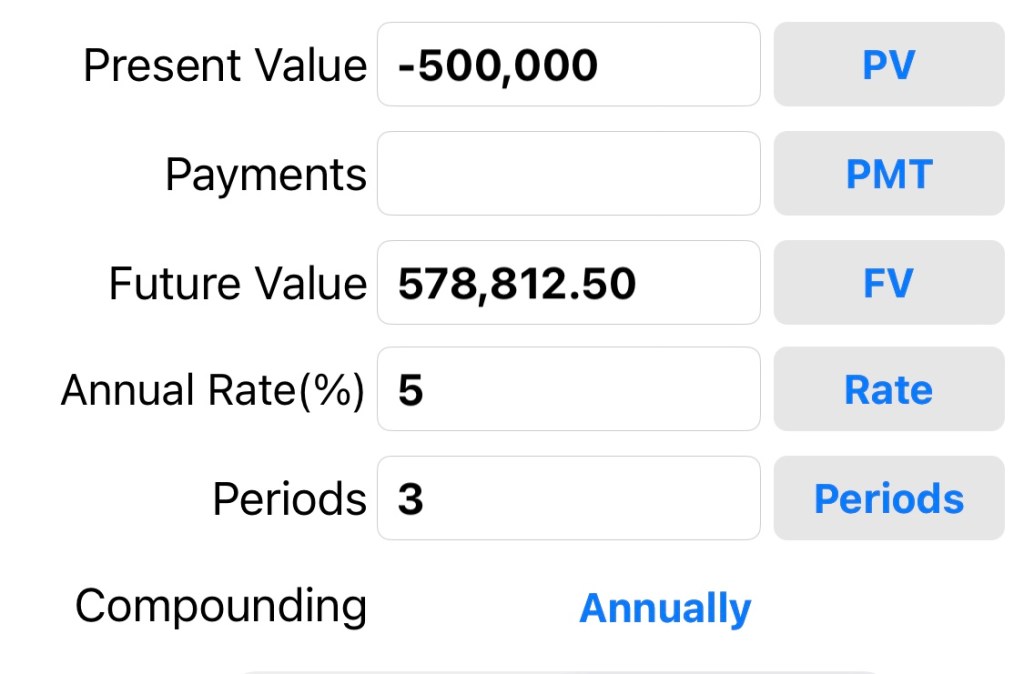

You spotted a Real estate investment $500k, 5% return p.a. for 3 yrs. Let’s say You draw from your $1m commercial bank. Your bank left $500k balance.

3 yrs later you make $79K profit.

Your bank interest earned in 3 years: $750.

Hence your total profit is $750+$79k: $80K

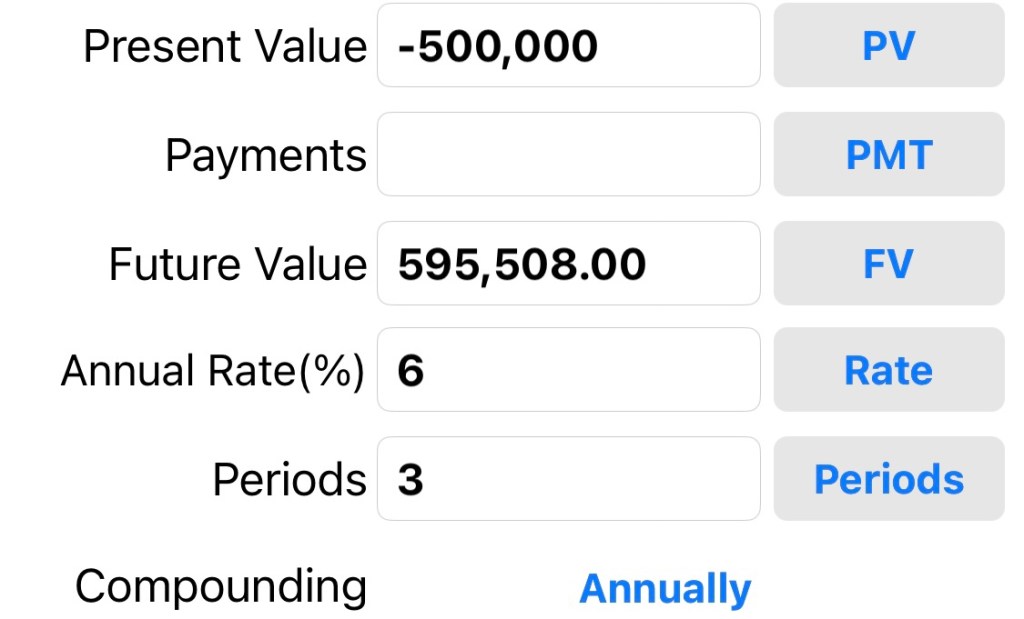

Now, Let’s try using the policy loan facility. Your own bank has $1m balance in terms of policy value. You borrow from insurer $500k and only pay back 3 year later in full.

Loan incurred: $96K

Profit from Real estate: $79K

Loss: $17,000 😱 oh dear, wrong move 😟😟😟

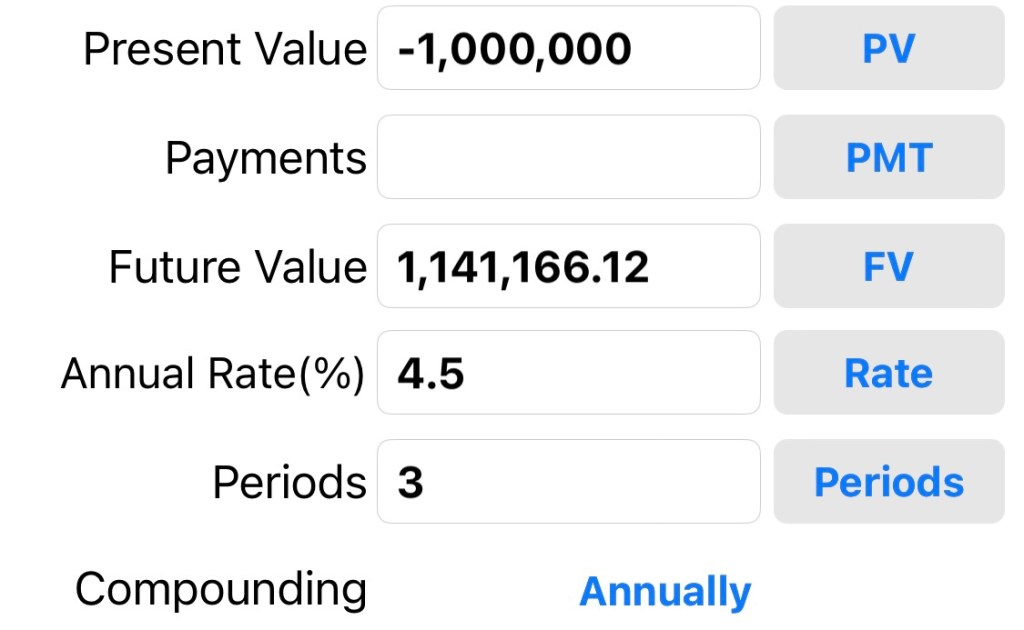

But your $1m cash in insurance is still growing in that 3 years remember?

Interest earned there: $141k.

Loss from real estate: $17k

Total profit: $124K 😉

Vs $79k if you use the “traditional” method.

In summary over here, we are not really advocating you to invest using policy loan for this particular scenario. Your low risk policy generates a decent 4-5% return, and it doesn’t make sense anyway for you to draw out to invest in a risky assets which yield you only 5%.

But even so, IBC method still trump traditional method because your policy value remain intact and continue to work hard for you, where as in commercial bank, you draw down your capital to buy, hence losing the already meaningless interest you suppose to earn.

Hence you would want to shift as much cash away from places like bank and start creating your own bank instead. Ideally, 90% in OWN BANK, and 10% in your commerical bank just for transactional purposes.

PS: Above scenario is assuming the person has no cashflow coming in in the next 3 years at all. In real situation, he has from working income, dividends & rental etc. And such cashflow should flow into paying back partially the policy loan, and hence the interest incurred is even lower, resulting in better yield for IBC METHOD.