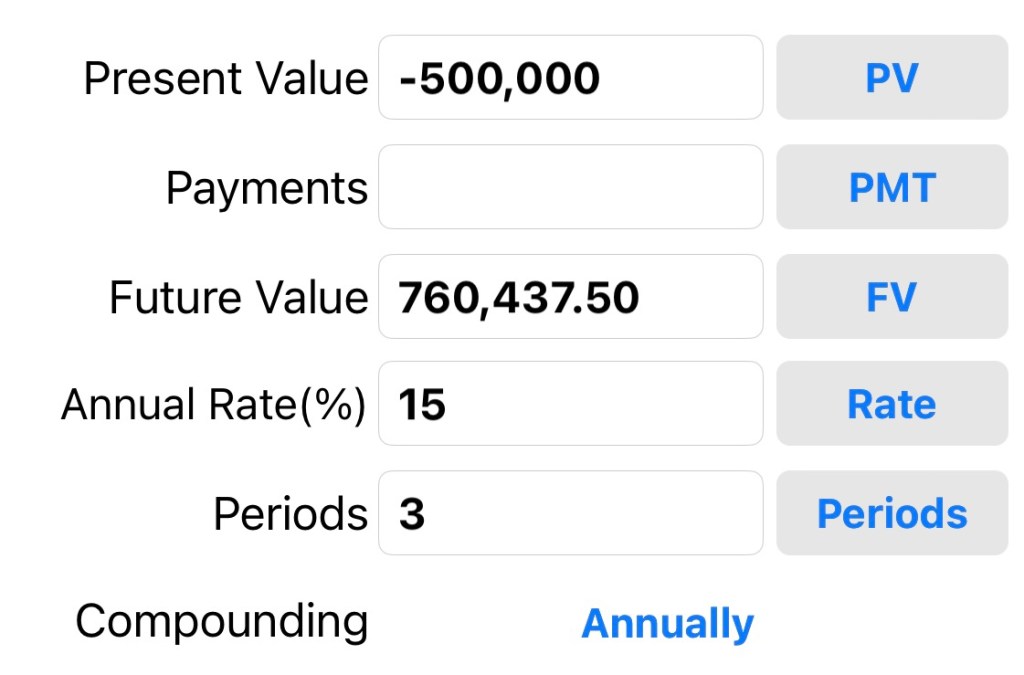

You spotted a Real estate investment $500k, 15% return p.a. for 3 yrs. Let’s say you draw capital from your $1m commercial bank balance. Your bank left $500k balance after the investment.

3 yrs later you make $260K profit.

There are some private real estate deal which I do know and indeed produces such returns. Will do a write up on it soon!

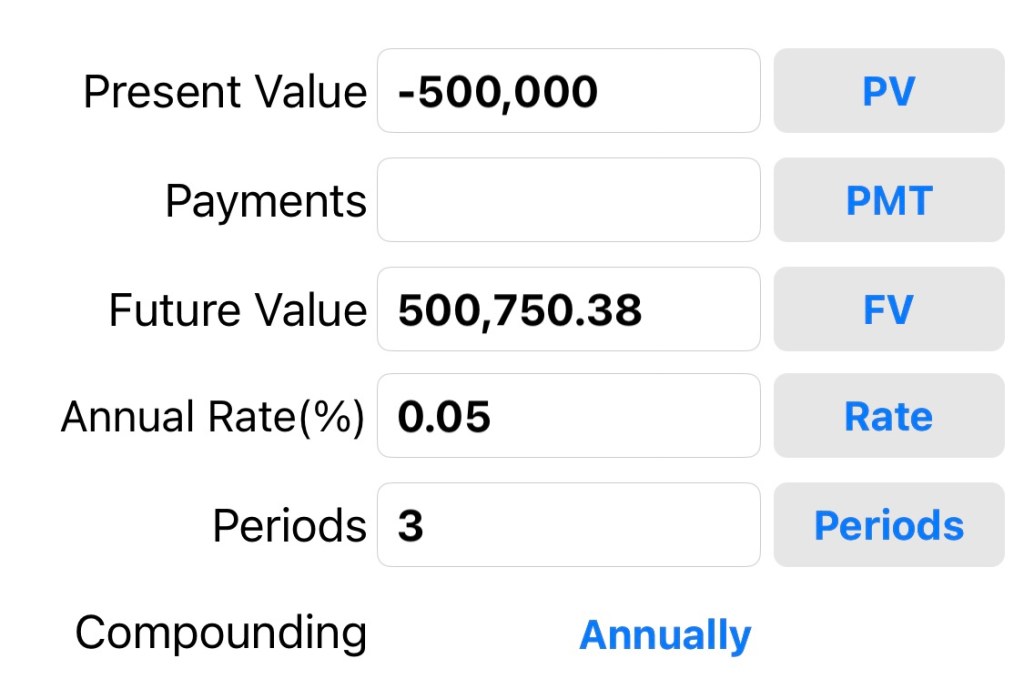

Your bank interest earned in 3 years: $750.

Hence your total profit is $750+$260k: $261K

As usual, bank is never going to give you more interest rate. In Japan, you have to pay them to deposit your money as it’s negative interest rate!

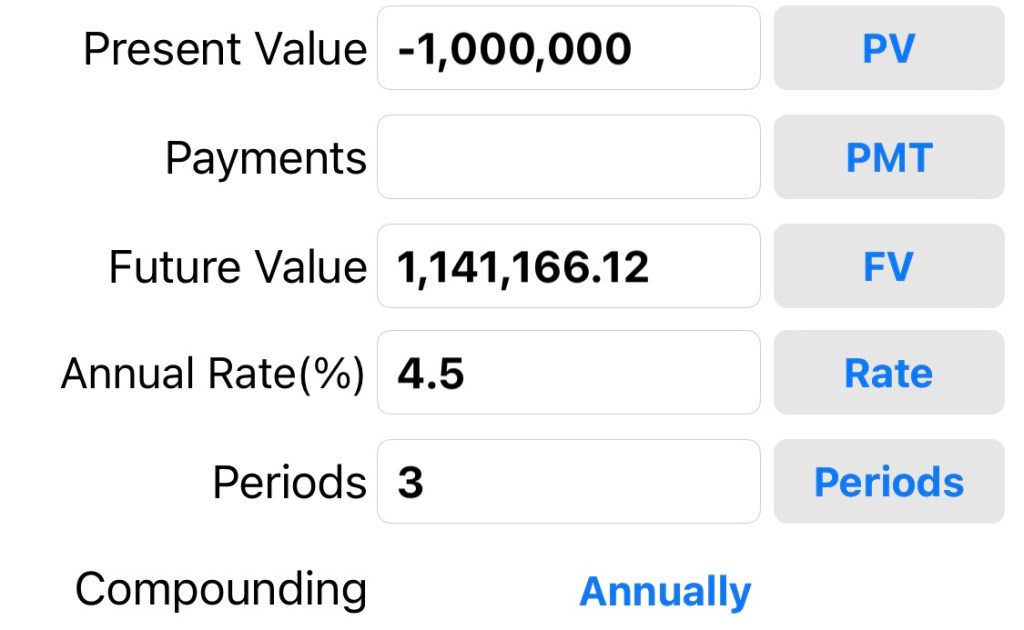

Now, Let’s try policy loan. Your own bank aka insurance policy has $1m balance in terms of policy value. You loan from insurer $500k and only pay back 3 year later in full.

Loan incurred: $96K

A typical policy loan interest rate is about 6% p.a. No processing fees, no early redemption fees, and no repayment schedule. You pay at your own time. Try bank loan, and if you don’t pay for a month, they are going to send you letters!

Profit from Real estate: $260K

Net profit: $164K

But your $1m cash in insurance is still growing in that 3 years remember?

Interest earned there: $141k.

To be able to accumulate to $1m policy cash value takes time, and of course a regular decent commitment in terms of premiums.

Net profit from real estate: $164k

Total profit: $305K

VS $261k if you use the “traditional” method.

In summary, we are not saying the loan facility by insurer is better in terms of loan interest cost. Trad. Bank OD facilities might be lower, albeit with certain risks.

But you would want to shift as much cash away from places like bank and start creating your own bank instead. Ideally, 90% in OWN BANK, and 10% in your commerical bank just for transactional purposes.

Essentially, You own this “bank”of yours. It’s guaranteed to grow in value over time. You can collateralise the equity in your bank and borrow money from the insurer anytime, with no repayment schedule required. You set your repayment yourself.

PS: Above scenario is assuming the person has no cashflow coming in in the next 3 years at all. In real situation, he has from working income, dividends & rental etc. And such cashflow should flow into paying back partially the policy loan, and hence the interest incurred is even lower, resulting in better yield for IBC METHOD.

Hi there! My name is Sam from Singapore, I have 3 young kids, namely Z, Q, & E. As of writing today, I have reached financial freedom, and I’m writing this blog to share my thoughts on financial matters, and anything related to money. Primarily, this blog is meant for ZQE as they grow up. While I hope I can grow together with them and pass down my values and tips to them, life can be unpredictable. Hence I hope this blog may come in handy for them in future, and since I’m writing it, I might as well share my thoughts to the world.

I came from a middle class family, and I’m fortunate that I have met great mentors in my life who selflessly shared their secret to me. Here I’m now, to share these secrets to you.

I have no get rich quick scheme for you though, and whatever I plan to share is basically fundamentals of financial planning. Amazon founder Jeff Bezos once asked Warren Buffett, “Your investment thesis is so simple. Why don’t more people copy you?” Buffet replied, “Because nobody wants to get rich slow.”

That’s the reason why I decide to name my site financial turtle!

You don’t have to be fast to be rich, nor you want to be slow as well. It isn’t about speed, it’s about consistency, and fully comprehending the 8th Wonder of the World; Compounding interest.

Hence I hope you find great ideas for you to implement on my site, otherwise thank you for viewing as the site was primarily built for my kids.

Disclaimer: whatever I share is purely based on my opinions, and if you have other thoughts, I welcome constructive feedback so that we can learn together.

Cheers!